By Sam Kwak. December 28th, 2023

So you may have heard from financial experts and gurus for years about paying off your mortgage early. But should you? Is this outdated advice or is it a timeless wisdom to pay off your mortgage faster? You might be wondering, what’s the smarter decision for me? Especially – with strategies and concepts like Accelerated Banking and Infinite Banking which are taught by the Kwak Brothers. So let’s dive first into the Pros and Cons of paying off your mortgage early versus using your cash to invest elsewhere. But also, we’ll discuss a perspective and an insight that many financial experts DON’T mention or consider when it comes to your 30-year mortgage.

PRO: Building Equity and Avoiding Overwhelming Mortgage Debt

Paying off your mortgage early can be a smart financial move that helps you build equity in your home and avoid overwhelming debt. In this blog post, we will explore the advantages of paying off your mortgage early and how it can contribute to your long-term financial well-being. Building equity and avoiding overwhelming debt are two important financial goals that can have a significant impact on your overall financial well-being. One of the primary advantages of paying off your mortgage early is the opportunity to build equity in your home. Equity is the difference between the market value of your home and the remaining balance on your mortgage. By paying down your mortgage faster, you increase the equity in your home and create a valuable asset that can be leveraged in the future.

There are several benefits to building equity in your home:

- Increased Net Worth: Building equity allows you to increase your net worth by increasing your ownership stake in your home.

- Borrowing Power: The equity in your home can serve as collateral for loans or lines of credit, providing you with additional borrowing power when needed.

- Financial Security: Having significant equity in your home provides a sense of financial security, as it can serve as a financial safety net during unexpected circumstances.

It is important to consult with a financial advisor or mortgage professional to determine the best strategy for paying off your mortgage early and building equity in your home.

PRO: The Dangers of NOT Paying Off Your Mortgage & Debt

While debt can be a useful tool for creating wealth and leveraging investments, it is essential to understand the dangers of overwhelming debt. Having too much debt can lead to a range of financial difficulties and negatively impact your financial well-being.

Here are some risks and consequences of overwhelming debt:

- Financial Stress: Overwhelming debt can cause significant financial stress and anxiety. The constant burden of high debt payments can impact your mental and emotional well-being.

- Higher Interest Payments: Carrying high levels of debt often means paying higher interest rates. This leads to more money going towards interest payments rather than building savings or wealth.

- Limited Financial Flexibility: When you have a significant amount of debt, your financial options become limited. It can be challenging to pursue new opportunities or make significant financial decisions, such as buying a home or starting a business.

- Credit Score Impact: Too much debt can negatively impact your credit score, making it more difficult to access credit or obtain favorable interest rates in the future.

Therefore, it is crucial to manage your debt responsibly and avoid taking on more debt than you can comfortably handle.

Then Is All Debt ‘Bad’?

While overwhelming debt can have negative consequences, debt can also be used wisely and smartly to create more wealth and leverage. So I’m not necessarily in the same ‘camp’ as some of the experts out there who say to cut off all credit cards and use only cash. Understanding the difference between good debt and bad debt is key to making informed financial decisions. Good debt is debt that is used to invest in assets that have the potential to appreciate or generate income. Examples of good debt include student loans for higher education, a mortgage for a home, or a business loan to start a profitable venture.

Bad debt, on the other hand, is debt incurred for non-essential items or depreciating assets that do not generate income. Credit card debt used for unnecessary purchases or high-interest loans for luxury items are examples of bad debt.

By using debt wisely, you can:

- Invest in Income-Producing Assets: Taking on debt to invest in income-producing assets, such as rental properties or a business, can help you build wealth and generate passive income.

- Take Advantage of Investment Opportunities: Debt can provide the leverage needed to take advantage of investment opportunities that have the potential for high returns.

However, it is crucial to establish a threshold and ensure that your debt remains within a manageable range. Continuously evaluate your financial situation and have a plan in place to pay down your debt efficiently.

CON: Then, What About Investing Instead?

So this is what I would consider to be a ‘Con’ of paying off the mortgage early. You may have heard advice that advocates for investing your dollars instead of using it to pay off your mortgage early. I am a strong believer in investing. Whether it’s stocks, bonds, mutual funds, index funds, ETFs, crypto, etc. I do believe in a strong and healthy habit of investing. I favor real estate over others but that’s just me, personally.

But the question is, if you’re using any savings and extra cash flow for investing, how do you pay off your mortgage early? It sounds like you have one choice.

I look at this decision from an opportunity cost perspective. Most people believe they need to make a decision purely based on the interest / ROI rate and this is where most people make the mistake when comparing investment vs. paying off your mortgage. You have to look at the actual cost of your mortgage as a whole as opposed to the potential return on investments.

So say, for example, you have a $100,000 thirty (30) year mortgage at a 5% interest rate And you have the opportunity to invest with a 7% return on investment. Looking at just the interest rate, it looks like ‘investing’ is the better choice. But let’s follow through on this by adding some real-life (Likely) scenarios. First, the total interest cost on our mortgage would be at $93,644. I used THIS calculator to help me calculate the cost of the interest over the 30 years. Also, remember that all mortgage interest cost is front-loaded which means that the vast majority of your interest cost is paid upfront as opposed to being linearly distributed equally. In other words, you don’t pay the same amount of interest every year.

Because we’re looking at the assumption of taking your extra cash flow each month to invest instead of paying off your mortgage, let’s assume you have about $1,000 each month to spare to invest. Let’s calculate your return on investment if we start investing $1000 a month with a 7% consistent return for the next 30 years. I’m going to use THIS calculator to help calculate the returns. After contributing about $30,000 of principal, you’ve earned approximately $71,073.04.

Now, if we apply the same $1,000 a month to our mortgage principal, you’ll notice the cost of interest goes down dramatically to $16,899. (I’m using the same calculator that I used to calculate the cost of the interest) We would have paid $93,644. The difference is $76,745.00. Looking purely at the cost of interest saved and the amount of money we could earn at 7% return, it’s clear that paying off our mortgage earlier would give us a net positive benefit. Now of course, if we would have assumed a higher return on investment, the math would favor investing instead. But you also have to consider the fact that higher investment returns could mean higher volatility and the potential for losses as well. On a particular year, you may even see double-digit returns. On the flip side, you might see double-digit losses. It happens!

So you must calculate the true cost of the interest and compare it to the true earnings potential of your investments. Comparing rates by itself doesn’t give you the accurate picture to help you make a well-informed decision.

But… Here’s Where Most Get Wrong About Paying Off Your Mortgage Early…

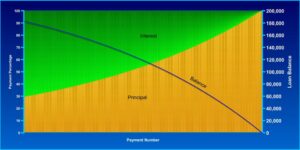

Here’s where it gets REALLY interesting about the cost of your mortgage. Remember how I said that your cost of interest is front-loaded? Meaning, that the vast majority of your interest cost is paid upfront, typically in the first 10 years. In fact, I wrote an entire article dedicated to what I’m about to explain.

(The image depicts a sample mortgage amortization chart to showcase the relationship between the principal and the interest per each monthly payment on a given month)

Now, let’s add that fact to what the U.S. Census Bureau data has to say about moving.

When it comes to moving, Americans are known for being quite mobile. On average, US adults move approximately 11.7 times in their lifetime. That’s a significant number of moves, with each relocation bringing about its own set of challenges and decisions to be made.

So there’s a bit of a conflict of interest here. (No pun intended). Let’s say you live to be about 80 years old. That means you’re likely to move every 6-7 years if we’re equally distributing the number of moves across your lifetime. You’ll notice that this is well within the front-loaded interest zone where the vast majority of your monthly mortgage payments are interest.

By the time you decide to move on the 7th year mark, you notice that you haven’t made significant progress with your mortgage principal balance because most of your payments have been interest. Yikes! When you sell your house to move and buy another, you often get a brand-new 30-year mortgage. As this occurs, you’re back to the cycle of mostly interest payments again for the next 7-10 years.

This vicious cycle of never-ending interest payments is another key factor as to why you may want to consider paying off your mortgage early or at least paying down a large amount of principal to accelerate the amortization schedule. This way, more of your monthly payments are reducing the principal balance as opposed to being interest.

Looking Beyond the Loan’s Lifetime

When most people consider the cost of their mortgage, they typically focus on the monthly payments and the interest paid over the life of the loan. While these are important factors, they don’t provide a complete picture of the true cost of your mortgage.

Our goal at Accelerated Banking and the Kwak Brothers is to help people understand the full lifetime cost of their mortgage, which takes into account additional factors such as inflation, potential changes in interest rates, and the opportunity cost of not utilizing that money for other investments.

By understanding the true cost of your mortgage across your lifetime, you can make more informed decisions about your financial future and potentially save thousands of dollars in the process.

Summary: The True Cost and Benefits of Paying off Your Mortgage Early

In summary, understanding the true cost of your mortgage over its lifetime is crucial for making informed financial decisions. By considering factors beyond just the loan’s lifetime, such as inflation and opportunity cost, you can gain a better understanding of the overall cost of your mortgage.

Paying off your mortgage early can help you save on interest payments and potentially reduce the total cost of your mortgage. This can provide you with more financial freedom and security, as well as the ability to allocate those funds towards other financial goals.

In conclusion, taking the time to understand the true cost of your mortgage and exploring options for paying it off early can have significant long-term benefits and help you achieve greater financial stability.

CLICK HERE to Learn How to Pay Off Your Mortgage In As Early As 5-7 Years

TL;DR:

Understanding the true cost of your mortgage over its lifetime is crucial. By considering factors beyond just the loan’s lifetime, such as inflation and opportunity cost, you can make more informed financial decisions. Paying off your mortgage early can save you on interest payments and provide financial freedom and security. It also allows you to allocate those funds towards other financial goals. Take the time to understand the true cost of your mortgage and explore options for paying it off early to achieve greater financial stability.